Trading in a financed car means selling your vehicle to a dealer while an auto loan is still active on it. The dealer pays off your remaining loan balance directly to your lender. If your car is worth more than what you owe, you pocket the difference as equity. If you owe more than it’s worth, that gap gets added to your next loan — or you pay it in cash.

What Does Trading In a Financed Car Actually Mean?

Trading in a financed car means selling your vehicle to a dealership while an active auto loan is still on it. The dealer pays your lender the outstanding balance directly. Any remaining equity is credited toward your next vehicle — or if you owe more than the car is worth, that difference is rolled into your new loan or paid upfront.

Let’s break that down even further.

When you finance a car, your lender holds a lien on the vehicle. A lien is basically a legal claim that says, “this car can’t be fully sold or transferred until the loan is paid.” The car is yours to drive — but it’s not 100% yours to sell until that lien is cleared.

Here’s what makes trading in different from just selling a car outright:

- You don’t have to pay off the loan yourself first. The dealer handles the payoff as part of the transaction.

- The process is legal and extremely common. According to Edmunds, roughly half of all new car purchases involve a trade-in — and a large share of those have outstanding loans.

- Your outcome depends on one key number: the difference between what your car is worth and what you still owe.

The four parties involved in every financed trade-in:

| Party | Their Role |

|---|---|

| You | Vehicle owner and borrower |

| Your lender | Holds the lien; receives payoff from dealer |

| The dealership | Buys your car, pays off your loan, sells you a new one |

| Your new lender | Finances your next vehicle (may or may not be the same lender) |

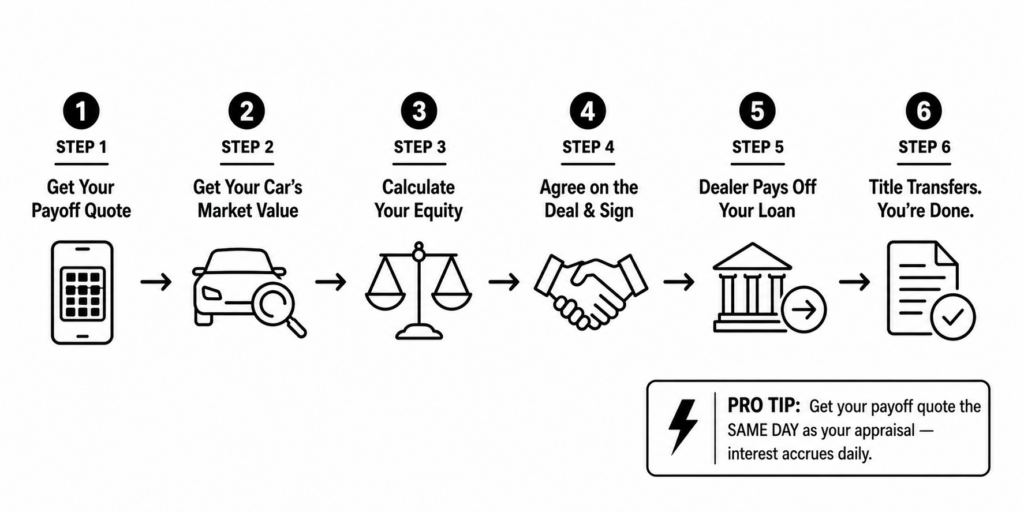

The 6-Step Process — Start to Finish.

Here’s exactly what happens when you trade in a financed car. This is the full sequence — from your living room to driving off the lot in something new.

Step 1: Get Your Official Loan Payoff Amount

Your payoff amount is NOT the same as your remaining balance — and this confusion costs people money.

Your monthly statement shows your principal balance. But the payoff amount also includes:

- Accrued daily interest up to the date the loan is actually paid off

- Any applicable fees (check your loan contract for early payoff clauses)

How to get your payoff quote:

- Log into your lender’s online account portal

- Call your lender directly (have your account number ready)

- Request a formal 10-day payoff letter — a written document valid for 10 business days

Major lenders like Chase Auto, Bank of America Auto Loans, and Capital One Auto Finance all offer online payoff tools. Credit unions typically require a phone call.

Step 2: Find Out What Your Car Is Actually Worth

The trade-in value is what a dealer will pay you for your car. It’s not the sticker price you see on used car lots — that’s the retail price. The trade-in value is closer to the wholesale price, typically $1,500–$4,000 lower than what you’d get selling privately.

Best free tools to check your car’s value:

- Kelley Blue Book (KBB) — The industry standard. Shows trade-in range and private party value side by side.

- Edmunds Instant Offer — Generates a real offer you can take to a dealer.

- CarMax Appraisal — Gives you a binding 7-day offer. Bring this to the dealership. It’s negotiating gold.

- Carvana and Vroom — Two more data points that take under 5 minutes each.

Step 3: Calculate Your Equity Position

This is the single most important calculation in any trade-in. Here’s the simple formula:

Equity = Trade-In Value − Loan Payoff Amount

A positive result means good news. A negative result means you’re “underwater” — you owe more than the car is worth.

We’ll go deep on this in the next section with real numbers.

Step 4: Agree on the Deal (Negotiate Smart)

One of the biggest mistakes buyers make: negotiating the new car price and trade-in value at the same time.

Dealers love this. It creates a fog of numbers where they can give you “more” for your trade while quietly raising the new car’s price.

The right order:

- Negotiate the purchase price of the new vehicle to your satisfaction — completely, before mentioning your trade.

- Then introduce your trade-in as a separate transaction.

- Compare the dealer’s trade offer against your CarMax/Edmunds benchmarks.

Step 5: The Dealer Pays Off Your Loan

Once you sign the paperwork, the dealership contacts your lender, verifies the payoff amount, and sends the funds — usually by check or wire transfer.

Here’s what happens behind the scenes:

- Dealer requests final payoff confirmation from your lender

- Funds are sent within 3–10 business days

- Your lender marks the loan as paid in full

- The lien is released — your lender no longer has a legal claim on the vehicle

- The title is transferred to the dealership (electronically in most states, or by mail)

Until your lender confirms receipt of the payoff, you are still responsible for your monthly payment. If a payment falls due in the gap between signing and dealer payoff — pay it. A missed payment shows up on your credit report regardless of the dealer’s timeline.

Step 6: Your Equity Gets Applied

- Positive equity → credited toward your new vehicle as a down payment, price reduction, or cash refund

- Negative equity → either paid in cash or rolled into your new loan balance

- Your old loan shows as “Paid/Closed — No Late Payments” on your credit report within 30–60 days

The Most Important Number: Your Equity Position

Before you do anything else, you need to know where you stand. Are you above water, below water, or right at the surface?

This single number determines everything — your options, your cost, and whether now is even the right time to trade in.

Three possible positions:

| Position | What It Means | What Happens |

|---|---|---|

| Positive equity | Car worth MORE than you owe | Difference credited to your next deal |

| Breakeven | Car worth roughly what you owe | Clean slate — nothing owed, nothing gained |

| Negative equity | Car worth LESS than you owe | Difference must be paid or rolled into new loan |

The Hidden Costs Nobody Warns You About

The Daily Interest Problem

Your payoff quote has an expiration date — usually 10 business days. Why? Because interest accrues on your loan every single day.

If the dealer delays sending the payoff past your quote’s expiration:

- Your lender will require a new, higher payoff quote

- The dealer is responsible for the difference — but you have to follow up to make sure it gets handled

- Always ask the dealer: “By what date will the payoff be submitted to my lender?” — and get it in writing.

How Trading In a Financed Car Affects Your Credit Score .

Your credit score isn’t dramatically impacted by a clean trade-in — but it’s not zero impact either. Here’s an honest, clear breakdown of what happens:

When Is the Best Time to Trade In a Financed Car?

Timing your trade-in strategically can mean the difference between walking in with leverage and walking in at a disadvantage. Two forces work against you in the early months of a loan: rapid depreciation and front-loaded interest.