You’ve found the house. You’re pre-approved. Your agent helped you craft a competitive offer — and now you’re staring at a screen wondering: who actually delivers this thing to the seller, and how does it all work?

It’s one of those behind-the-scenes details that nobody really walks you through until you’re in the middle of it, and the last thing you want is to be caught off guard when a dream home is on the line.

Here’s the good news: once you understand the offer delivery framework — who does what, in what order, and why — the whole process feels a lot less like a black box. This guide lays it all out, from choosing your delivery path based on your specific situation, to what happens in the crucial hours after your offer lands on the seller’s table.

Key Takeaways

In most U.S. home purchases, your buyer's agent delivers your offer to the seller's listing agent — not directly to the seller.

If you don't have a buyer's agent, you can submit your offer directly to the listing agent or seller (as in FSBO transactions), but having a real estate attorney is strongly advised.

Dual agency — where one agent represents both buyer and seller — is legal in most states but illegal in nine, including Texas, Colorado, and Florida.

A complete offer package includes your signed purchase offer, pre-approval letter, earnest money details, contingencies, and optionally a personal buyer's letter.

After delivery, sellers typically respond within 24–72 hours with one of three outcomes: acceptance, a counteroffer, or rejection.

The Key Players You Need to Know

Before walking through the framework, let’s get clear on who’s in the room — or at least on the email chain. According to the National Association of Realtors (NAR), a typical residential real estate transaction involves four main parties:

The buyer (you): You’re making the offer, arranging the financing, and hoping to get the keys. Every decision in the offer delivery process ultimately starts and ends with you.

The buyer’s agent: A licensed real estate professional who represents your interests exclusively. They help you write the offer, advise on pricing strategy, and handle all formal communication with the other side. NAR data consistently shows that over 85% of recent home buyers purchase through a real estate agent or broker — so this is still by far the most common path.

The listing agent: This is the seller’s agent. They are legally obligated to act in the seller’s best interest — not yours. Everything your buyer’s agent submits goes through this person before it ever reaches the seller.

The seller: The current homeowner who will review and decide on your offer. In most transactions, the seller doesn’t receive your offer directly — they hear about it from their listing agent, who frames and presents it on your behalf.

Understanding this chain of representation matters because it drives every step of the framework below.

The Offer Delivery Framework: 4 Steps to Follow

Think of this as a decision map. The path you take depends on your situation, but the destination is always the same — getting your offer in front of the seller in the strongest possible form.

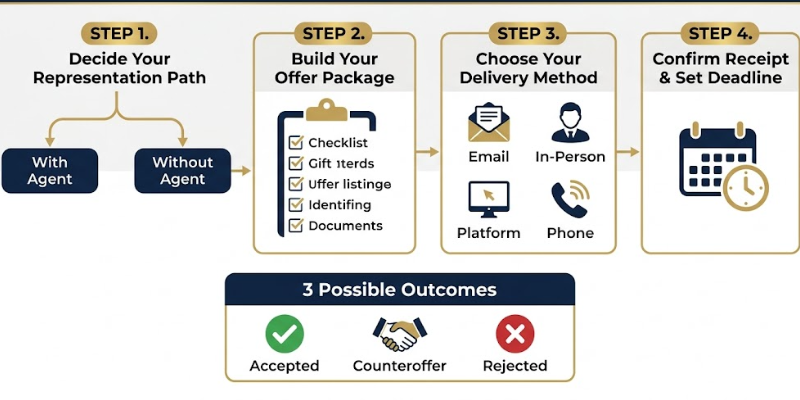

Decide Your Representation Path

This is the fork in the road that shapes everything else.

If you have a buyer’s agent (the most common scenario): Your agent takes the wheel. Once you’ve reviewed and signed the offer, they submit it — along with all supporting documents — directly to the listing agent. Your agent may also place a quick call to the listing agent beforehand, giving them a professional heads-up that a strong offer is coming. In competitive markets, that relationship-building call can make a real difference before the seller even opens an email.

If you don’t have a buyer’s agent: You’ll deal with the listing agent or the seller directly. This happens most often in For Sale By Owner (FSBO) transactions, which account for roughly 7% of U.S. home sales. Without representation, you take on the full burden of negotiation, paperwork, and due diligence yourself. In this case, a licensed real estate attorney isn’t just advisable — it’s essential. They can review your purchase contract, flag unfavorable terms, and protect you if anything goes sideways before closing.

Build a Complete Offer Package

Delivering an offer isn’t just sending over a number. It’s presenting a complete package that gives the seller every reason to say yes. Here’s what a strong offer package should include:

- A signed purchase offer with your proposed price, preferred closing date, and all agreed-upon terms. The Consumer Financial Protection Bureau (CFPB) outlines what a legally sound purchase agreement should contain — worth a quick read before you sign.

- Your mortgage pre-approval letter — not a prequalification, which carries far less weight. Lenders issue pre-approval after verifying your income, assets, and credit history. Bankrate explains the difference clearly if you need to sort out where you stand.

- Earnest money details — the good-faith deposit you’re prepared to make, typically 1%–3% of the purchase price, held in escrow until closing.

- Contingencies — standard real estate contingencies include inspection, financing, and appraisal. Waiving them can strengthen your offer in a competitive market, but it carries real financial risk. Never waive a contingency without fully understanding what you’re giving up.

- A personal buyer’s letter — optional, but in emotionally charged sales, a short genuine letter about why you love the home can tip a close decision in your favor. That said, some listing agents discourage buyer letters because they can inadvertently reveal demographic information, raising Fair Housing Act compliance concerns. Let your agent read the room on this one.

The cleaner and more complete your package, the faster the listing agent can present it — and speed matters, especially in fast-moving markets.

Choose the Right Delivery Method

There’s no single official channel for submitting an offer. Your agent will use whatever method gets it delivered fastest and most reliably. Here’s what that looks like in practice:

Email with e-signature platforms: This is today’s standard. Tools like DocuSign, Dotloop, and Authentisign create a legally binding, timestamped record of every action taken — critical when multiple offers are competing and minutes can matter.

In-person delivery: Less common but still used. Showing up in person signals urgency and seriousness, and if your agent has an existing relationship with the listing agent, that face-to-face moment can set your offer apart before the seller reads a single word of it.

Offer management platforms: Many brokerages now use dedicated software portals for offer submission, giving listing agents a dashboard to present multiple offers to sellers side by side in a clean, comparable format.

Phone call followed by formal submission: In fast-moving markets, your agent may call the listing agent first to signal intent and ask strategic questions — then formally submit the package immediately after. This pre-submission conversation can surface whether competing offers are already in play and whether an escalation clause would be worth including (more on that in Pro Tip #1 below).

Confirm Receipt and Set a Response Deadline

Once your offer is transmitted, your agent should confirm receipt with the listing agent. This isn’t just professional courtesy — it’s strategic. That quick follow-up also opens the door to valuable intelligence:

- When does the seller plan to review offers?

- Are there competing offers already on the table?

- Has the seller set a formal offer deadline buyers should know about?

Just as important: your offer should include its own expiration window — typically 24 to 72 hours. This creates appropriate urgency without being aggressive, and prevents your offer from sitting in limbo while the seller waits for a better bid. Nolo’s real estate legal guide notes that a clearly stated response deadline is one of the most overlooked but impactful elements of a buyer’s offer — and one that protects both parties.

What About Dual Agency? Know the Rules in Your State

Dual agency occurs when a single real estate agent — or two agents from the same brokerage — represents both the buyer and the seller in the same transaction. It happens most often when a buyer reaches out directly to the listing agent after finding a home online or at an open house.

In theory, the dual agent is supposed to remain neutral. In practice, it’s a structurally compromised arrangement — the agent has a prior relationship with the seller, knowledge of both parties’ positions, and a financial incentive to close the deal regardless of who bends. Most experienced buyers’ advocates advise against it.

More critically, dual agency is illegal in nine U.S. states: Alaska, Colorado, Florida, Kansas, Maryland, Oklahoma, Texas, Vermont, and Wyoming. If you’re buying in any of these states, you are legally entitled to your own independent representation. The NAR Code of Ethics addresses agent conflicts of interest directly — and any agent attempting dual agency in a prohibited state isn’t bending a rule, they’re breaking the law.

If you’re unsure about your specific state’s rules, HUD’s housing counselor locator can connect you with a certified professional who can advise you on your rights at no cost.

Timing your offer submission strategically can give you a real edge. Research from Zillow consistently shows that homes attract the most activity and competing offers in their first 7–10 days on the market. Submitting early — ideally within the first 48 hours of a listing going live — signals to the seller that you're prepared and serious. On the flip side, avoid submitting late on a Friday or over a holiday weekend. Agents and sellers are harder to reach, acknowledgments are delayed, and your offer can lose momentum before anyone reads it.

What Happens After Your Offer Is Delivered?

Once the listing agent presents your offer to the seller, one of three outcomes follows:

Your offer is accepted. You’re officially under contract. Congratulations — now the real work begins. Expect to submit your earnest money deposit within a few days, schedule a professional home inspection, and keep your financing on track. The CFPB’s closing checklist is a practical tool for staying organized through this phase. One important rule: avoid any major financial changes — new credit accounts, large purchases, or job changes — between contract and closing. Lenders re-verify your financial status right before funding, and surprises at this stage can kill your loan.

The seller makes a counteroffer. A counter is not a rejection — it’s an invitation to negotiate. The seller may push back on price, closing date, contingencies, or personal property inclusions like appliances or fixtures. Your agent will help you evaluate the counter and respond in a way that protects your interests while keeping the deal alive. Nolo’s counteroffer guide walks through your options and rights at this stage.

Your offer is rejected. It stings, but it happens — especially in markets where sellers receive multiple strong competing bids. Always ask your agent to find out why: was it price, terms, financing strength, or simply a better-positioned buyer? That feedback sharpens your next offer directly. And don’t close the door completely — if the seller’s first-choice buyer falls through during inspection or financing, they may come back to you. Staying professionally visible through your agent costs nothing and occasionally wins you the house on the rebound.

Frequently Asked Questions

Can I deliver my offer directly to the seller, bypassing the agents? Not advisably — and in most cases, not appropriately. If you have a buyer’s agent, all formal communication is supposed to flow through the agents on each side. Contacting the seller directly can create legal liability, damage your credibility in the transaction, and violate the terms of your representation agreement. The clear exception is FSBO situations, where there’s no listing agent and direct seller communication is standard.

Does the seller personally read my offer? The listing agent typically reviews the offer first, then presents it to the seller — sometimes in person, sometimes via a digital summary. In busy markets where sellers receive many competing offers, agents often present key terms in a side-by-side comparison format. Your buyer’s letter and any notable terms — like a large earnest money deposit or flexible closing date — will typically be highlighted.

How long does a seller have to respond to my offer? As long as — or as short as — your offer specifies. There is no universal legal default deadline. Most offers include a 24–72 hour response window, and you should absolutely define one. Cornell Law School’s Legal Information Institute explains how offer expiration functions as a matter of contract law — without a stated deadline, an offer can remain technically open indefinitely, leaving you in limbo.

What is an escalation clause, and when should I use it? An escalation clause automatically increases your offer above competing bids by a fixed increment, up to a cap you define. Use it when competing offers are likely and you’re genuinely committed to the home. The trade-off is transparency — the seller will know your maximum. Investopedia’s escalation clause explainer covers how to structure one and what protections to build in before you sign.

If my offer is rejected, can I resubmit? Yes — and it’s often worth doing. Ask your agent what drove the rejection. If it was price or terms, you may be able to come back with a revised offer that lands better. If the seller accepted another bid and that deal falls apart during due diligence, you could be next in line. Staying professionally engaged through your agent costs nothing and sometimes turns a rejection into a deal.